The Conversation (0)

GearBrain

Bitcoin and the bandits: Have we returned to the cryptocurrency Wild West?

Bitcoin is experiencing wild price increases

Booming prices, multi-million dollar heists, confusion over fake applications plus exchanges bombarded by new users hungry to make a quick buck — the bitcoin Wild West is back.

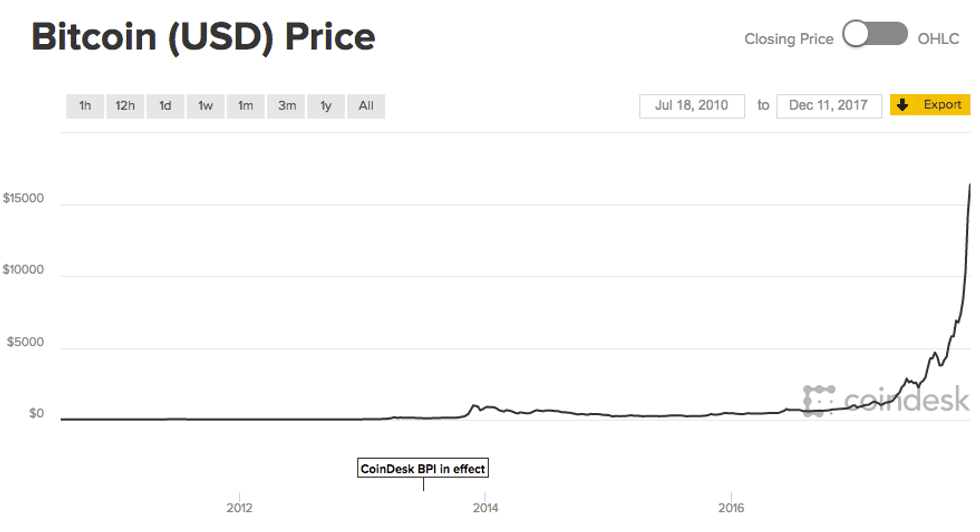

Bitcoin was worth around $780 per coin, one year ago. The currency remained relatively stable since the last major boom and bust of 2013, where prices hit the heady heights of $1,000 per coin. Now bitcoin is worth in excess of $16,500, as 2017 draws to a close.

Such rampant growth — up from $2,000 in July and at one point climbing at a rate of over $300 per minute — has, as always, attracted new investors. These investors have seen the Winklevoss twins become, on-paper, billionaires thanks to buying into bitcoin. New investors want a piece of the action.

Unfortunately, this has several consequences. The first is the cryptocurrency network's inability to cope with floods of new users all trying to create accounts at once. The blockchain technology on which bitcoin is built can manage for now. But the exchanges, which let you buy bitcoin, litecoin, ethereum and others for regular currencies like dollars and euros, buckle under the load.

The most well-known, Coinbase, has suffered several outages through 2017. Sometimes this is due to publicity around bitcoin's soaring worth encouraging new users to flood the servers; other times it is bitcoin's falling value and panic selling which causes the outages.

Bitcoin's value has surged by over $10,000 in the last monthCoinbase

Bitcoin's value has surged by over $10,000 in the last monthCoinbase

Coinbase's profile and reputation for being the easiest way to buy and sell bitcoin, saw it become the most downloaded app on the US iOS App Store in early December, reports TechCrunch. The app then stumbled and fell offline as 300,000 new customers tried to open accounts in a single day.

But unless Coinbase falls offline during a crash in bitcoin's value — preventing traders who've lost their nerve from selling — bitcoin's value and Coinbase's servers will likely recover.

At the time of writing, Coinbase is the 20th most popular free iOS app in the US, just two places behind WhatsApp and ranking above Twitter and Chrome.

Volatility

Cryptocurrency is, at its most simple, a form of virtual money or a digital means of payment which does not rely on a central bank. The currency is mined digitally by doing work — having a computer run through a series of actions for which it's rewarded with virtual funds. Cryptocurrency transactions are authenticated by computers linked to the blockchain, which acts as a public ledger and a permanent record of every transaction. As these computers authenticate transactions, they 'mine' more currency, which is distributed between those used to mine it.

Most people, however, buy bitcoin and other cryptocurrency on exchanges, like Coinbase.

Cryptocurrencies are exchanged directly between two people — or between a buyer and seller, or a buyer and a business — and offer an almost entirely anonymous way of making and receiving payments online. Of the different cryptocurrencies, bitcoin is considered to be one of the best known, first appearing in 2009.

A serious side effect of bitcoin's rampant growth is the risk volatility that it can pose to retailers. Listen to bitcoin's biggest fans and they will tell you how cryptocurrencies are the future of money and a better alternative to centralized banking, as the funds can be transferred directly from one person to another — or from one person to a business, supplier or retailer. When bitcoin first gained mainstream attention in 2013 and 2014 it was heralded as the future of online money, and some websites and online services began accepting it as payment.

But now bitcoin's extreme volatility is scaring retailers away again. Steam, the online video game store, announced this month it would no longer accept bitcoin payments "due to high fees and volatility."

The company added how bitcoin transaction fees, which it has no control over, have "skyrocketed" from around $0.20 when Steam enabled bitcoin payments, to $20. "These fees result in unreasonably high costs for purchasing games when paying with bitcoin," it added.

Bitcoin spent its first three years below $100Coindesk

Bitcoin spent its first three years below $100Coindesk

Add in extreme volatility, and Steam has called time on bitcoin. "It has become untenable to support bitcoin as a payment option. We may re-evaluate whether bitcoin makes sense for us and for the Steam community at a later date," the company added.

This move suggests the very point of bitcoin, to act as a currency enabling owners to pay for goods and services, is at risk because it is instead being treated as a highly fluctuating commodity. And more than that, it is a fluctuating commodity which has a history of rewarding lucky investors with enormous — and almost entirely unpredicted — gains.

Even before the boom in late-2017, early investors who'd cashed in their coins for houses in 2016 had fueled the belief that buying bitcoin will make you rich.

Only this week, bitcoin futures became tradable on the Chicago Board Options Exchange (CBOE), the world's largest futures exchange, and prices quickly jumped by 10 percent.

Bitcoin and the bandits

Bitcoin's surging value and anonymous, digital nature make it a prime target for cyber criminals looking to catch out new cryptocurrency businesses, exchanges and users who haven't done their homework. The most recent victim was Slovenia-based NiceHash, a bitcoin mining service which sold computer processing power to customers who wanted to mine the currency. On December 6 the company was subjected to a four-hour attack in which it lost 4,736 bitcoins, worth between $60m and $70m.

NiceHash chief executive Marko Kobal said: "A hacker or group of hackers were able to infiltrate our internal systems through a compromised company computer. We're still conducting a forensic analysis on how he affected computer was actually compromised."

A single bitcoin began the year at $970, yet is now over $16,000

A single bitcoin began the year at $970, yet is now over $16,000

Bitcoin heists are not rare. In November, a cryptocurrency trading startup called Tether had $31m stolen from its digital wallet.

Reuters claims there have been at least three dozen heists on cryptocurrency exchanges since 2011, including the infamous theft of 850,000 bitcoins from Mt Gox in 2014, leading to its collapse. In all, almost one million bitcoins have been stolen from exchanges, worth in the region of $16B today. Precious few have been recovered.

Inexperience in cryptocurrency doesn't just apply to fledgling startups and investors keen to buy a slice of the action. Apple was caught out this month, as an app pretending to be MyEtherWallet appeared on the iOS App Store. Not only did the app — which claimed to offer a wallet service for ethereum and other cryptocurrencies — make it into Apple's strictly monitored walled garden, it stayed there for a week and reached third place in the store's finance apps category.

The $4.99 app is the work of a developer with no history of cryptocurrency, but has made three other apps — two of which feature fighting pandas. At the time of writing, GearBrain can no longer find the app in question.

2018 and beyond

At this point we should try and make a prediction for what 2018 has in store for bitcoin and the rest of the cryptocurrency landscape. But history tells us this would be foolish. All we can say with a modicum of certainty is that bitcoin's volatility will continue to spook retailers who accept it as payment. If more follow Steam's lead, bitcoin will keep riding its self-perpetuating rollercoaster away from usable currency and closer to Wild West commodity.

Disclosure: The author of this article owns approximately $440 worth of bitcoin.

GearBrain Compatibility Find Engine

A pioneering recommendation platform where you can research,

discover, buy, and learn how to connect and optimize smart devices.

Join our community! Ask and answer questions about smart devices and save yours in My Gear.